by Parvathi Bakshi

According to Morningstar, “FinTech companies are those businesses that leverage technology to create better and perhaps new financial services both for consumers and businesses. It includes companies of all kinds that may operate in personal financial management, insurance, payment, asset management, etc.”

Overall, technology disruption in the financial services industry, has improved back-end systems by creating secure means to process sensitive data, as a result of which mobile banking apps and e-payment platforms have gained significant prominence. Investors are jumping to invest in not only totally new ideas but also invest in business which are combining traditional services with new tech. Generally changes in supply and demand economics can be understood if we look at the behavioural changes of customers. As such, the general attitude of customers (especially the millennials) towards financial apps has also proved to be a factor promoting innovation and investments in fintech. Further as more countries are seeing their populations come ‘online’ and have access to basic internet via their phones, the possibilities for providing financial services to a larger market have increased. For example, in India, demonetization, GST and a focus on financial inclusion through digital inclusion, has seen the population shift to using mobile financial services such as Paytm, Google Pay, DigiLocker and mobile banking apps (Lee, 2019).

Market Trends in FinTech: 2013-2020

Globally, from 2013 to 2019, fintech funding went from a little under $19bn to a little over $133bn and digital payments have been the largest component of fintech as per the Pulse of FinTech 2018 and 2019 Report. An improved attitude of customers towards accepting technology to deliver reliable financial services has translated into a demand for further integration of tech in finance.

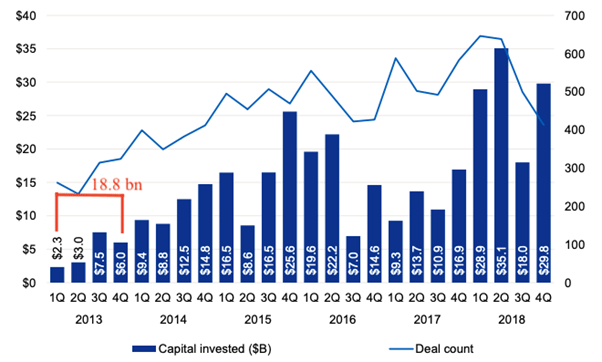

Graph 1 here pulled from the KPMG reports, shows the starting growth in capital investments in 2013. There is a sharp jump in the Q3 of 2013 to $7.5bn from $3bn, with banking and payments leading the distribution, followed by data analysis and personal financial management (Statista, 2014).

Graph 1. Total investment activity (VC, PE and M&A) in fintech 2013-2018, Source: Pulse of Fintech 2018, Global Analysis of Investment in Fintech, KPMG International (data provided by PitchBook) January 4, 2019.

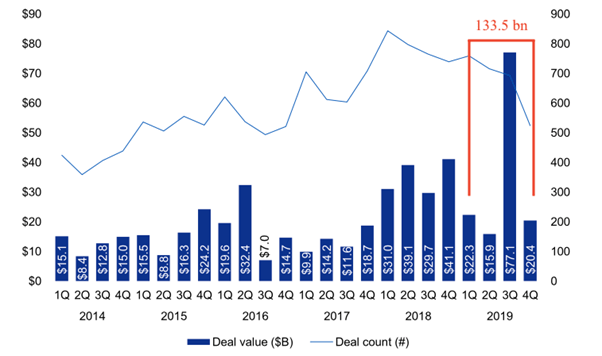

Graph 2 shows a whopping $133.5bn in investments and a huge portion of Q3 was due to Fidelity National Information Services’ $42.5bn acquisition of Worldplay.

Graph 2. Total investment activity (VC, PE and M&A) in fintech 2014-Q4 2019. Source: Pulse of Fintech 2019, Global Analysis of Investment in Fintech, KPMG International (data provided by PitchBook), as of 31 December, 2019.

The black swan of 2020 i.e. Coivd-19, brought global investment in fintech to a halt, with most of the completed deals being those from 2019. However, the first half of 2020 still saw over 1000 deals valuing up to $25.6bn, with payments and lending sectors seeing strategic deals getting done with a greater focus on increasing use of APIs and open data (KPMG, 2020). Despite the slowdown, growth stage companies and start-ups continue to attract significant investments.

Is millennial attitude driving demand?

The discussions on trends in fintech would be incomplete without discussing millennials (those born in the ‘70s to ‘90s). Millennials play a key role in the upcoming growth of financial industries partly because of the wealth they will be inheriting and their ability to adopt technology quickly. According to Nielsen’s ex-CEO Mitch Barns, millennials are no longer the future but they are the here and now (Nielsen, 2018). They are hyper connected via the internet and have access to far more choices of products and services. However this level of hyper connectivity where they have access to so much information also results in fragmentation in their consumption choices.

Market volatility of course has had its role in influencing millennials and a recent example is the 2008 Financial Crisis. Having experienced such a crisis, it’s no surprise that trust of financial institutions is minimal amongst this cohort, which also translates into high risk aversion in financial investments. They are far less trusting and have a somewhat sceptical view of financial advice and services. While they may be optimistic about their futures, many other factors such as societal challenges, environmental degradation and general mistrust of governments and large MNCs drastically impact their investment decisions (Deloitte Global Millennial Survey 2019). An interesting observation is seeing this generational shift away from traditional financial investment strategies by older generations towards impact investing, driven by the millennials desire to have a better future. While this cohort is drastically diverse and may not necessarily act as predicted, this article looks at the common trends among millennials and the common factors that drive the behaviours associated with millennials.

Impact Investing

Impact investing refers to financial investments in businesses which will have a positive or at least, minimal negative impact on the society, environment or political situation. This manner of investing aims to do away with purely profit making motives and introduces elements of compassion in financial investments. Popular social impact investments could include investing in startups which focus on producing biodegradable products for packaging or investing in micro-finance companies which extend loans to women in war-torn countries. Essentially impact investing aims better social, economic or political outcomes alongside with financial return.

Millennials being the socially, culturally and politically diverse lot that they are, have tended to choose investments based on the specific impact such as social or environmental impact. Seen as a way to express their social and political viewpoints, millennials rely on the societal impact and ethics of a company when determining their relationships with that company or business (Deloitte, 2019). They are also the same cohort among the other generations, such as Boomers and the Silent Generation, who are far more entrepreneurial and more likely to be self-employed. Thus we see millennials not only investing in ‘ethical businesses’ but also starting their own business, based on the very same ideals driving their investments. So how does this translate for fintech companies and innovators? Well, behavioural characterises such as (a) self-optimism (b) mistrust of others (c) inclination towards social betterment and (d) technology adaptability, has been the driving force of fintech. And the robo-advisory space is gaining popularity among millennials primarily because of their use of big data to customise investing strategies for their clients, which is attractive to a millennial looking for impact investing. Companies like Acorns, Stash and Robinhood are developing apps that making investing easier (Lulic, 2020), by utilising cost-efficient and transparent strategies to attract millennials. While robo-advisors are customising investment from individual to individual – allowing millennial clients to easier pick and chose their brand of impact investing. While these are just a few examples of fintech startups and companies, many other players are riding on the hopes that millennials will stick to their values of ethical, compassionate and not purely profit driven investment strategies.

Conclusion

As seen from the graphs, fintech is a rapidly growing industry and the role of technology as a disruptor has been welcomed by a growing market of millennial consumers. The shift away from traditional methods of rendering financial services has been largely due to new millennial attitudes, risk aversiveness and tendency to look at social/political/environmental impact. On the technology side, the millennials’ ability to adopt technology has driven incumbents to become more flexible in the way they offer their services. To conclude, we can see that millennials are indeed driving the demand side of the fintech market and a 2018 CB Insight survey report showed that over 70% of the surveyed millennials, were more likely to look for financial offerings from tech companies like Google and Amazon than their nationwide bank (Lulic, 2020). So even though the Covid-19 pandemic may have hampered some of the market growth, the supply-demand relationship between fintech companies and millennials will shape the evolution of financial industry in the next quarter of the 21st century.